viper-zero/iStock Editorial via Getty Images

FedEx (NYSE: FDX) reported on 25.th in June and exceeded analysts’ expectations for revenue and earnings. In December 2023, I assigned FedEx stock a Buy rating, and while that rating has not produced above-average returns, but the performance numbers are slightly skewed. In this report I will discuss:

- Development of the FedEx share price.

- Result Q4 2024

- The financial forecast for the 2025 financial year

- My price target and my valuation for FedEx shares.

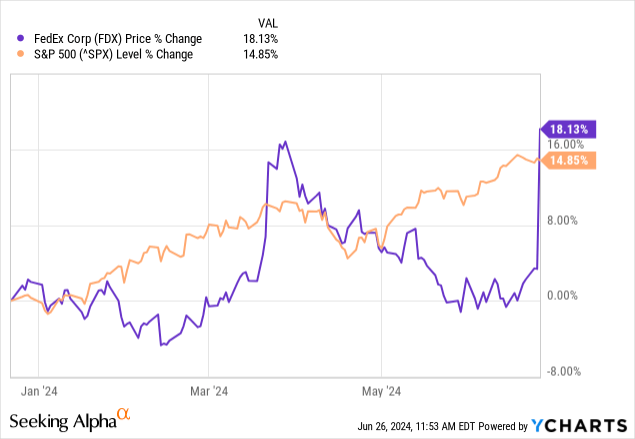

How has FedEx’s share price performed?

Interestingly, as I was writing this report, the stock price hit my previous price target of $293 and is now outperforming the market. The share price is up 18.1% compared to a 14.9% return in the broader markets.

I edited this section before submitting to include a comment to the significant increase in share prices, but would also like to reiterate my previous comment, which reflects FedEx’s share price before the significant increase:

Since I rated FedEx stock a Buy, the stock has only risen 3.37%, compared to 15% for the S&P 500. This is obviously not the kind of performance we expect from stocks we rate as Buys. The reason for the stock’s poor performance is the crash that followed the release of its third-quarter earnings. Before that, 95% of the upside I expected had occurred. So the stock was only 5% below my price target before falling again. FedeEx stock tends to fall quite sharply when there are concerns about performance and market conditions, and that is the main reason for the rather poor performance, even though the stock has come very close to my price target.

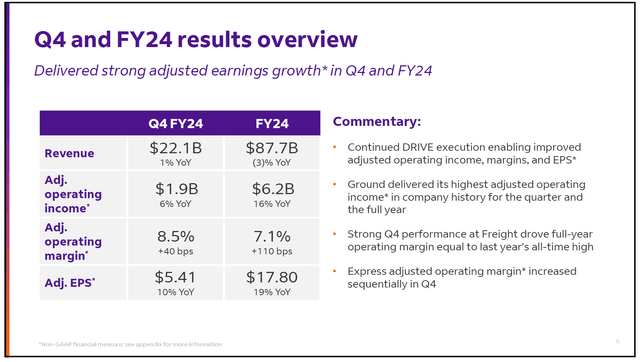

FedEx beats analysts’ estimates for revenue and profit

In the fourth quarter, FedEx reported revenue of $22.1 billion, beating analyst estimates by $40 million. Looking at the relative size of the overachievement, I would consider it more likely that revenue was in line with estimates or only slightly above. Earnings per share were $5.41, beating estimates by $0.04. This overachievement was relatively small, so I don’t consider fourth quarter earnings to be a real driver of the stock price.

FedEx

However, the fourth quarter and full year results showed something to be very pleased with, namely the fact that the company reported stronger growth in its adjusted operating income on slightly higher revenues in the fourth quarter and lower revenues in fiscal 2024. This can be seen as confirmation that the implementation of the DRIVE program is well on track. The DRIVE program aims to permanently reduce costs by $4 billion by fiscal 2025. Driven by this cost-cutting initiative, the company has been able to increase its profits in a very challenging freight and logistics market. So far, the company has achieved $1.8 billion in savings, including $500 million in savings in the Air Network & International segment, $750 million in savings in the Surface Network and another $550 million in savings in general and administrative expenses. So the company is halfway there and the simple conclusion is that further cost savings are possible, which offers a strong outlook.

FedEx

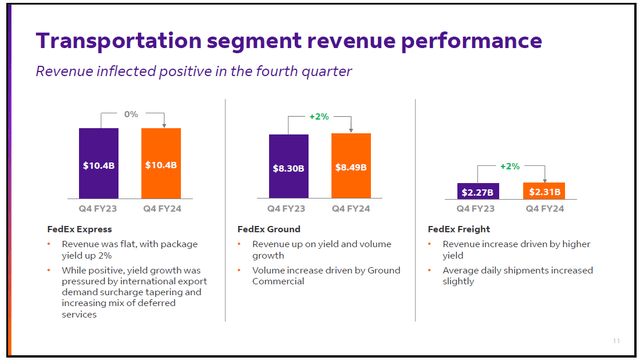

FedEx Express revenues remained stable despite package yield increasing and positive international package volume growth year-over-year while domestic package volumes declined. Revenues remained stable as positive package yield and positive international volume were offset by lower domestic package volumes, lower international demand surcharges and higher deferred services in the revenue mix. Deferred services are the cost-effective delivery solutions for businesses and these are less expensive, so having more of these services in the mix will obviously have a negative impact on revenues.

FedEx Ground revenues increased 2%, driven by a combination of volume growth and favorable yields. FedEx Freight saw revenues increase 2%, driven by slightly higher volumes but primarily by higher yields. Year-over-year, yields for domestic, ground and freight services increased slightly, while for international parcels they decreased due to lower surcharges as international capacity increased significantly as more commercial aircraft returned to service, improving utilization and therefore capacity.

FedEx

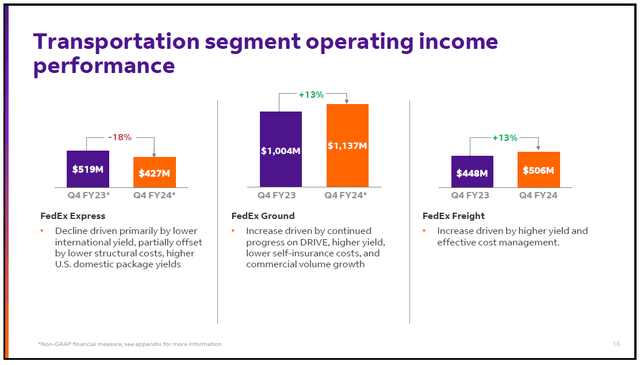

Looking at the segment’s operating profit, it’s not really surprising that FedEx Express’ results declined 18%. This was due to the aforementioned international network challenges, partially offset by cost-cutting initiatives. The Express segment also recorded transportation costs for the rollout of the Tricolor initiative. The Tricolor initiative is part of the DRIVE initiative to optimize Asst utilization. The purple network aims to move high-priority and large volumes through FedEx’s own fleet and network, the orange network is more of a point-to-point network to offload FedEx hubs and connect to ground-to-surface networks, while the white network serves as an adaptive capacity layer served by FedEx partners.

The company took a $157 million impairment charge related to the removal of 22 Boeing 757 freighters and seven engines from the U.S. domestic network. This write-down is reflected in non-GAAP reporting, but it is important to remember that FedEx is adjusting its capacity to meet demand and modernizing its fleet. While results are declining, margins improved from 2.8% to 4.1%.

FedEx Ground increased its segment results by 13%, or $133 million, due to higher yields, lower insurance costs and volume growth. At the same time, the DRIVE initiative is paying off, resulting in a margin increase of 130 basis points to 13.4%. FedEx Freight also saw a 13% increase in profits, due to revenue and cost management. In the ground and surface network, we are also seeing a shift to rail to maximize efficiency.

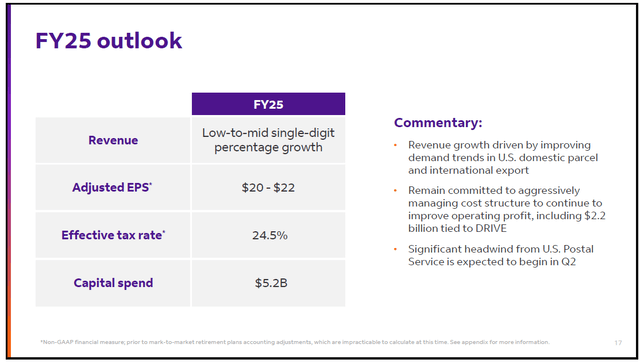

FedEx predicts a bullish year

FedEx

For fiscal 2025, FedEx has provided a very strong outlook that has driven the stock price significantly higher following the earnings release. There is a positive inflection point in domestic and international demand trends that will result in low- to mid-single-digit revenue growth, while capital expenditures will remain flat year-over-year and represent a lower percentage of revenue. For the full year, operating income is expected to increase by $1 billion despite several headwinds.

The additional revenue is expected to generate only $0.1 billion in additional profits. That is not enough to offset the $1.3 billion headwinds. In September, FedEx’s contract with the US Postal Service will be terminated, which will generate $0.5 billion in headwinds. The company has not yet outlined exactly how this will be mitigated, but we are already seeing capacity adjustments and I believe the expiration of the contract will allow the company to further size the fleet and improve operational efficiencies. Another headwind is $0.4 billion as international export yield remains under pressure, and then there is another $0.3 billion due to fewer operating days and $0.1 billion due to variable compensation. The offsetting factor is not the expected revenue growth, but the additional $2.2 billion in DRIVE savings that need to be achieved. A big driver of the savings appears to be improvements in operational efficiencies in Europe, where there is a $600 million savings potential. From the conference call, we could not determine exactly to what extent the cost reduction has already occurred, but it is probably still at an early stage, as the company sees great optimization potential in Europe.

So the guidance is really strong and that’s primarily due to the DRIVE initiative initiated by FedEx, which will more than offset $1.3 billion of headwinds, just as it offset the operational challenges in fiscal 2024.

FedEx shares remain a buy

The Aerospace Forum

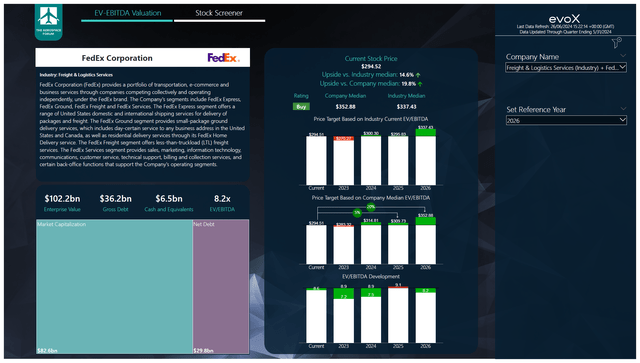

I have added the most recent results, guidance and balance sheet data to the evoX Stock Screener and maintain my Buy rating. The FY25 price target would be around $210, representing around 5% upside. However, given DRIVE’s solid execution and the fact that the company is already operating in FY25 at the time of writing, one could also assume the FY26 price target of $353, representing 20% upside. Interestingly, while FY24 results were quite strong, multi-year EBITDA generation is now expected to be around 3% lower as international demand premiums are expected to continue to decline. Free cash flow generation is expected to be stable compared to my previous forecasts and this is due to ongoing challenges in international markets and costs absorbed for network transformation before being offset by lower capital expenditure. We have also increased our net share repurchase assumptions, which are expected to be $500 million higher than previously modeled, while the company will likely be able to continue increasing dividends.

Wall Street analysts have projected an average price target of $308.15 for FedEx, which is in line with the FY25 price target shown in my stock screener. I believe that given DRIVE’s strong guidance and strong execution, we will see a price increase and move closer to the FY26 target I calculated.

Conclusion: FedEx is on a growth path

The fiscal 2024 and fourth-quarter results are clear evidence that FedEx’s targeted cost-cutting efforts are paying off. In fact, the savings outweigh the headwinds, and that’s definitely a good sign. The company also has good prospects for further cost reductions in fiscal 2025, with large cost reductions expected to be realized in Europe. Fiscal 2025 will again be a year of various headwinds, but the DRIVE initiative will again mitigate those headwinds. We’re seeing some positive developments in revenue and volume, but the reality is that international revenue will continue to be present, which will likely lead to further surcharge cuts. When you consider all of the various headwinds and tailwinds and couple them with FedEx’s valuation, I believe FDX stock remains a buy.