Municipal bonds ended the month and the first half of 2024 quietly ahead of the July 4th-shortened week, with new issuance totaling a measly $240 million—though there was plenty to watch beyond that.

Munis outperformed U.S. Treasuries on Friday, holding steady while Treasuries took some losses and stocks were weaker toward the close after May consumer data came in largely as expected, further underpinning expected future actions from the Federal Reserve, one day after the first U.S. presidential debate.

As for the former, “PCE inflation is gradually declining but is still above the Fed’s 2% target,” noted Mercatus Center macroeconomist Patrick Horan in his analysis of May PCE inflation data. “I would not expect today’s data release to change the Fed’s thinking on rate cuts. For now, we should not expect a rate cut before September.”

The market is now giving the Fed “the green light to consider a rate cut at its September 18 meeting,” said John Kerschner, head of US securitization products at Janus Henderson Investors. “While Federal Reserve officials are likely to stick to their guns in the coming weeks and say they are ‘data dependent,’ we will be watching closely to see if they try to downplay these rate cut expectations or perhaps even reiterate them.”

“We have two rounds of inflation data left before this meeting, and it is becoming increasingly likely that the data on easing inflation will give the Fed the backing to start cutting rates later this year,” Kerschner added.

Markets reacted less to the headline-grabbing debate between President Joe Biden and former President Donald Trump on Thursday.

“The US electorate remains polarized and we expect a major debate about whether investment portfolios should be reviewed,” noted Solita Marcelli, Chief Investment Officer Americas at UBS Global Wealth Management. “However, we believe that abruptly adjusting long-term financial planning in the wake of a single debate carries its own risks and could ultimately prove counterproductive.”

A greater impact on the public finance industry, at least in the short term, may come from the U.S. Supreme Court’s ruling this week that held that the Securities and Exchange Commission (SEC) cannot conduct administrative litigation in cases where it seeks civil penalties.

Other Supreme Court decisions to note are Loper Bright Enterprises v. Raimondo and Relentless, Inc. v. Department of Commerce, The court ruled against the so-called Chevron doctrine, which allows federal agencies to rely on their own rules and interpretations.

For participants focused on public finances, markets saw a “significant” rise in U.S. Treasury yields this week, “mainly due to strong auctions as well as a plunge in the yen to its lowest level since the mid-1980s,” strategists at Barclays PLC said in a weekly report. “Tax-free U.S. Treasury yields have moved broadly in line with tax-exempt U.S. Treasury yields.”

However, the municipal bond market “successfully fought its way through a strong primary market in June, with the municipal-to-government bond ratio remaining relatively tight,” BofA Global Research strategists said in a weekly report.

In fact, the

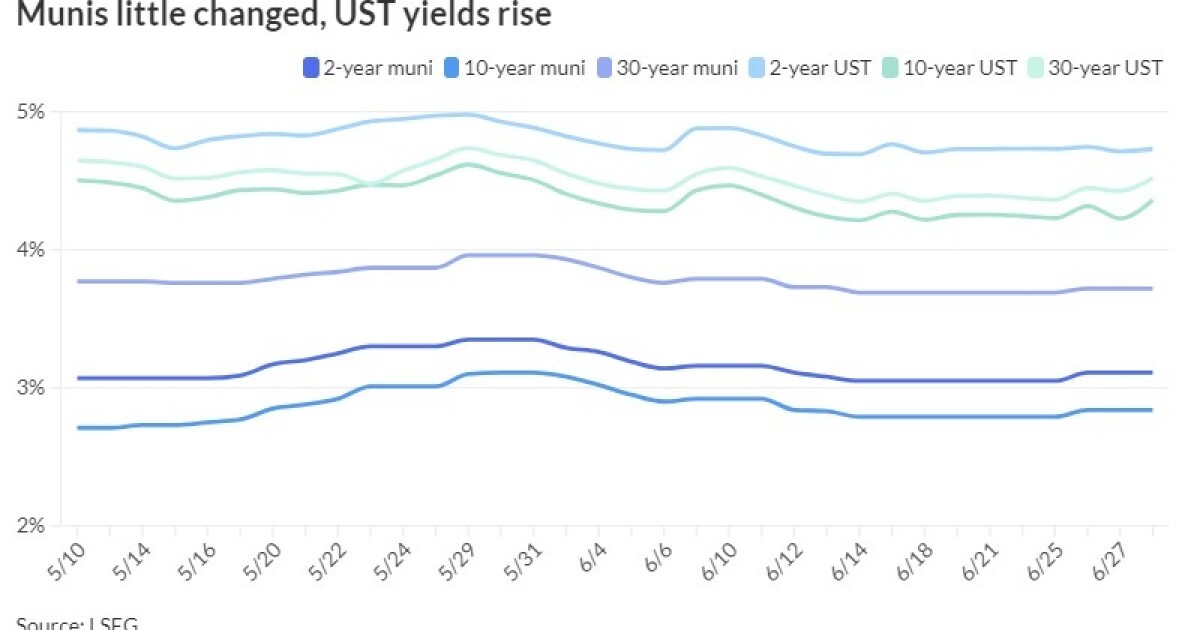

After Friday’s moves, the ratios were little changed: The two-year municipal bond to Treasury bond ratio was 66%, the three-year bond to Treasury bond ratio was 66%, the five-year bond to Treasury bond ratio was 67%, the 10-year bond to Treasury bond ratio was 65% and the 30-year bond to Treasury bond ratio was 84%, according to Refinitiv Municipal Market Data at 3 p.m. EST. ICE Data Services reported the two-year bond to Treasury bond ratio was 66%, the three-year bond to Treasury bond ratio was 67%, the five-year bond to Treasury bond ratio was 68%, the 10-year bond to Treasury bond ratio was 68% and the 30-year bond to Treasury bond ratio was 84% at 3:30 p.m.

“As we enter July, the supply/demand dynamics will shift significantly in favor of bond investors,” said BofA strategists Yingchen Li and Ian Rogow.

BofA expects to issue $37 billion in new long-term bonds in July, “which will be significantly exceeded by $65 billion in redemptions and coupon payments,” it said. “We view the current caution in the municipal market as a good opportunity to take positions ahead of our expected 100 basis point rally in the second half of 2024.”

Barclays expects issuance of at least $30 billion in July, noting that July will be the month with the highest redemptions this summer, “and not just for high-denomination bonds; redemptions in Puerto Rico are likely to be close to $1.5 billion,” said strategists Mikhail Foux and Clare Pickering.

They expect technicals to support the market in early July, “even if yields continue to rise as expected and interest rate volatility persists.”

Despite this week’s sell-off, yields on U.S. Treasury bonds fell by about 20 basis points in June, “which helped the municipal bond market,” Barclays said.

They noted that top-rated BBBs again performed better, but AAAs also did well, “though they are still down for the year.” Single-A and double-A parts of the market underperformed this month, they said.

Bloomberg Municipal Index yields on Friday morning show munis up 1.51% in June, while still down -0.43% for 2024. High yield bonds, on the other hand, have returned 2.46% so far in June and 4.15% for 2024. Taxable munis are +1.59% for June and +0.45% for 2024.

AAA scales

Refinitiv MMD’s scale remained unchanged: the one-year maturity was 3.15% and the two-year maturity was 3.11%. The five-year maturity was 2.88%, the ten-year maturity was 2.84% and the 30-year maturity was 3.72% (as of 3 p.m.).

The ICE AAA yield curve was little changed: 3.19% (unch) in 2025 and 3.11 (unch) in 2026. The five-year yield was 2.92% (unch), the ten-year yield was 2.88% (unch) and the 30-year yield was 3.72% (unchanged) at 3:30 p.m.

S&P Global Market Intelligence municipal yields were unchanged: The one-year yield was 3.17% for 2025 and 3.11% for 2026. The five-year yield was 2.88%, the 10-year yield was 2.88% and the 30-year yield was 3.70% at 3 p.m.

Bloomberg BVAL remained unchanged: 3.17% in 2025 and 3.12% in 2026. The five-year bond was at 2.93%, the ten-year at 2.84% and the 30-year at 3.73% (as of 3:30 p.m.)

Government bonds were weaker.

The yield on the two-year UST was 4.726% (+1), the three-year UST was 4.522% (+3), the five-year UST was 4.341% (+4), the ten-year UST was 4.355% (+7), the twenty-year UST was 4.616% (+8) and the thirty-year UST was 4.514% (+9) at 3:40 p.m.