Warren Buffett once said, “Volatility is far from synonymous with risk.” So it is obvious that you need to consider debt when thinking about how risky a particular stock is, because too much debt can ruin a company. Inter Action Corporation (TSE:7725) does have debt, but should shareholders be concerned about its use of debt?

Why is debt risky?

Debt helps a company until it struggles to pay it back with either new capital or free cash flow. If things go really bad, lenders can take control of the company. A more common (but still painful) scenario, however, is that new equity must be raised at a low price, permanently diluting shareholders. The benefit of debt, of course, is that it often represents cheap capital, especially when it replaces a company’s dilution with the ability to reinvest at high returns. The first step in looking at a company’s debt levels is to look at its cash and debt together.

Check out our latest analysis for Inter Action

How much debt does Inter Action have?

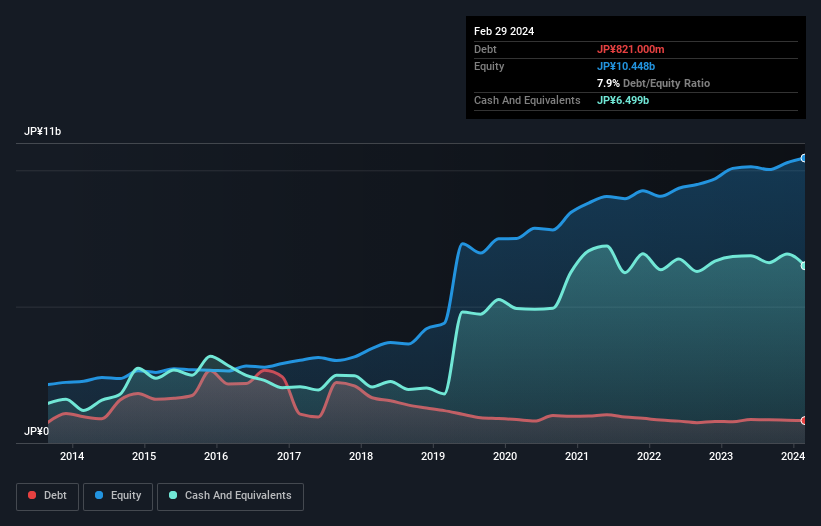

The image below, which you can click on for more details, shows that Inter Action had JP¥821.0 million in debt as of February 2024, up from JP¥777.0 million a year earlier. However, the balance sheet shows that the company holds JP¥6.50 billion in cash, so it actually has JP¥5.68 billion net.

A look at Inter Action’s liabilities

According to the last reported balance sheet, Inter Action had liabilities of JP¥1.53 billion due within 12 months and liabilities of JP¥470.0 million due beyond 12 months, compared with JP¥6.50 billion in cash and JP¥1.88 billion in receivables due within 12 months. This gives Inter Action JP¥6.38 billion more cash than in total Liabilities.

This ample liquidity means that Inter Action’s balance sheet is as robust as a giant sequoia tree. Given this, you might assume that the company’s balance sheet means it is able to weather some adversity. In short, Inter Action is net cash flowing, so it’s fair to say that the company does not have a heavy debt load!

The modest debt load could become crucial for Inter Action if management cannot prevent a repeat of last year’s 38% cut in EBIT. Falling profits (if the trend continues) could make even modest debt quite risky, after all. There is no doubt that we learn the most about debt from the balance sheet. But it is above all future profits that will determine whether Inter Action can maintain a healthy balance sheet going forward. So if you are focused on the future, you can look at free Report with analysts’ profit forecasts.

After all, a company can only pay off its debt with cold hard cash, not accounting profits. While Inter Action has net cash flow on the balance sheet, it’s still interesting to see how well the company converts its earnings before interest and tax (EBIT) into free cash flow, as this affects both its need for debt and its ability to manage it. Looking at the last three years, Inter Action recorded free cash flow of 41% of its EBIT, which is weaker than expected. This weak cash conversion makes debt difficult to manage.

Summarize

While we understand investors who are concerned about debt, keep in mind that Inter Action has net cash of JP¥5.68b as well as more cash than liabilities, so we have no problem with Inter Action’s use of debt. The balance sheet is clearly the area to focus on when analyzing debt. However, not all investment risk is contained on the balance sheet – quite the opposite. To that end, you should be aware of the following: 3 warning signs we discovered it at Inter Action.

Ultimately, it’s often better to focus on companies that have no net debt. You can access our special list of such companies (all with a track record of earnings growth). It’s free.

Valuation is complex, but we help simplify it.

Find out if interaction may be over- or undervalued by checking our comprehensive analysis which includes Fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View free analysis

Do you have feedback on this article? Are you concerned about the content? Get in touch directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Valuation is complex, but we help simplify it.

Find out if interaction may be over- or undervalued by checking our comprehensive analysis which includes Fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View free analysis

Do you have feedback on this article? Are you interested in the content? Contact us directly. Alternatively, send an email to [email protected]