Sergei Dubrovskii/E+ via Getty Images

introduction

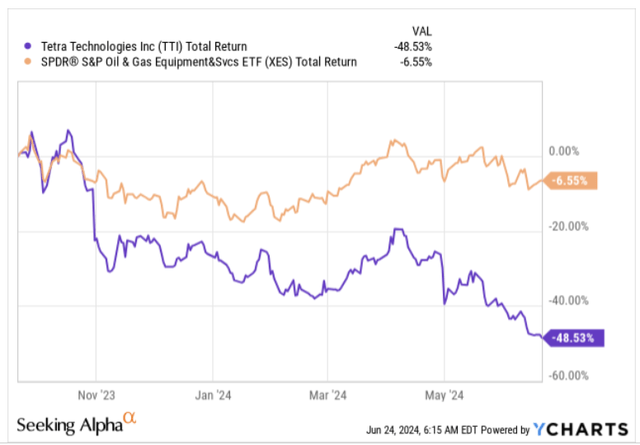

In September 2023, we wrote an introductory article about Tetra Technologies, Inc. (NYSE: TTI), a small cap stock known for providing various energy services and solutions across the globe (more than 13 countries). In our previous article, we talked about some of the the basic subplots of the TTI story, but we weren’t too keen on going long as the risk/reward ratio on the charts wasn’t all that enticing. Over the last nine months, the stock hasn’t performed particularly well, underperforming its peers in the oil and gas equipment services universe by more than seven times!

YCharts

This recent period of underperformance may have spooked some investors, but we still think there’s a lot to admire about TTI’s story. Here are a few reasons why we think it’s a good idea to get into TTI.

Operational improvements

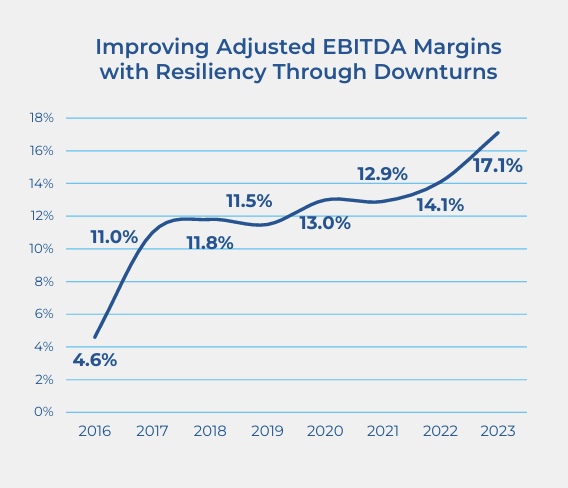

One of The standout reasons to choose TTI are the company’s ability to eliminate inefficient costs from the business, double down on automation and also move into high margin business opportunities. While there have been some setbacks along the way, we can see the long-term trajectory of the margin profile is on the upside. This year, management has stated that increasing margins remains “their strategic priority for 2024.”

Q1 Investor Presentation

Admittedly, the Group’s EBITDA margins suffered a setback in the recently concluded first quarter due to some seasonal and one-off effects in the Water and Flowback Services segment (which accounts for half of the Group’s revenue). However, the outlook for the rest of the year is expected to be much better: margins for this segment are expected to reach the mid-teens (they were 9.6% in the first quarter).

It is also worth noting that the water and flowback business has traditionally been a very labor-intensive business, but TTI has made efforts to increase the level of automation while reducing the labor burden. Currently, they have increased the level of automation in this business to 50% and the goal is to bring it to 100% by the end of the year.

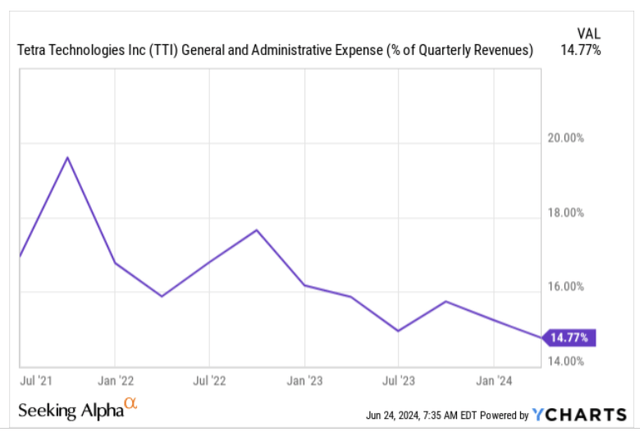

Also consider how much the company spends on administrative expenses each quarter. About three years ago, they invested almost 20% of their revenue in this area; over time, this percentage has steadily declined and is now less than 15%.

YCharts

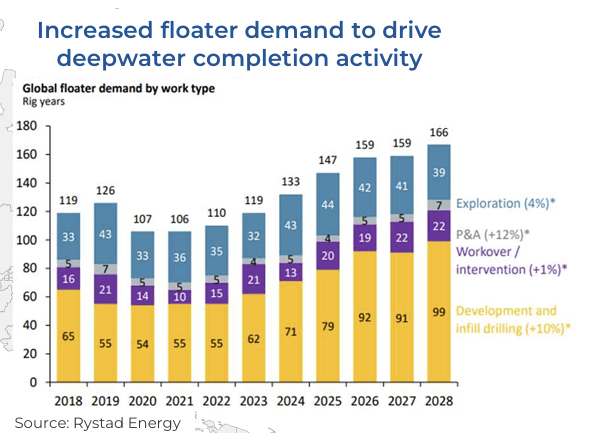

In addition, it is also worth highlighting the increasing demand for some of TTI’s high-density bromine-based completion fluids, which are inherently high margin. Much of this is related to strong deepwater development activity in the Gulf of Mexico, which is on track to generate another 500,000 barrels more than current volumes (for comparison, approximately 70% of deepwater drilling in the Gulf of Mexico uses bromine-based completion fluids). Rystad Energy now expects that demand for floaters could increase by an average of 10% per year in drilling years through fiscal 2026, which would be a useful catalyst for TTI’s completion fluids.

Q1 Investor Presentation

Forward valuations now appear attractive

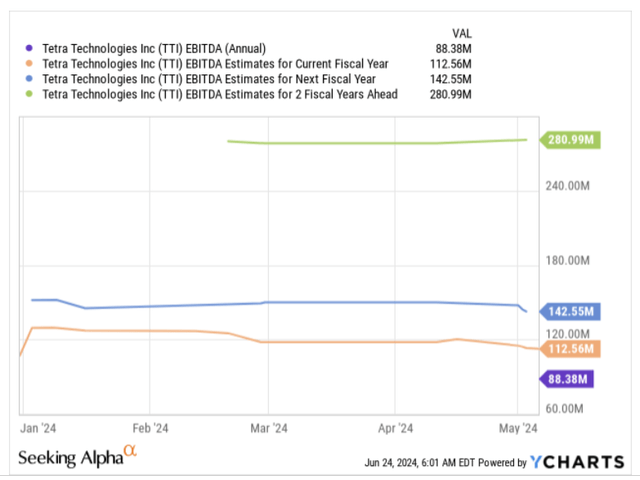

Overall, it is important to note that TTI’s EBITDA trajectory will improve dramatically in the coming years. Essentially, we could achieve a very healthy EBITDA CAGR of 47% between FY 2023 and FY 2026.

YCharts

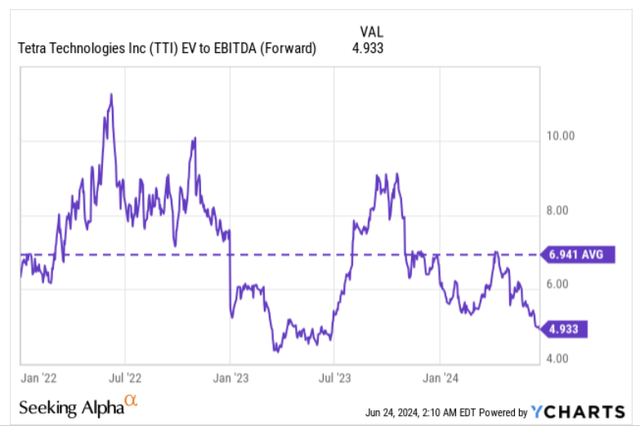

For a company that generates such EBITDA growth over the medium term, an above-average EV/EBITDA ratio would not be unusual. However, this is not the case with TTI.

YCharts

Rather, TTI is currently trading at an EV/EBITDA of less than 5x, which represents a 29% discount to the long-term average.

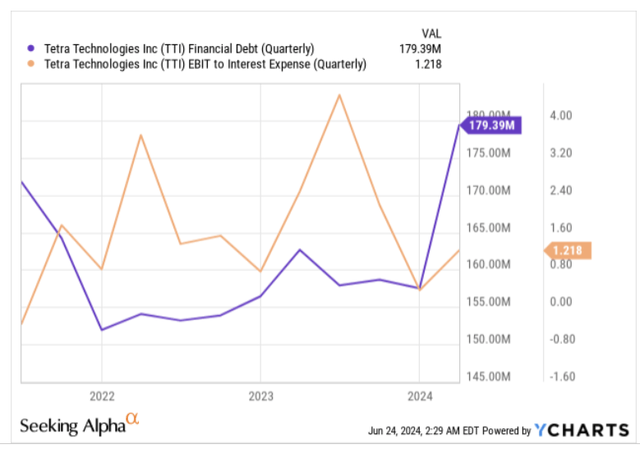

Now, some cynics may be wondering whether we will see a similar increase in earnings per share (EPS) given the likely increase in interest costs, as TTI’s debt level is now at its highest in three years at $179 million and interest coverage has fallen from over 4x to just over 1x.

YCharts

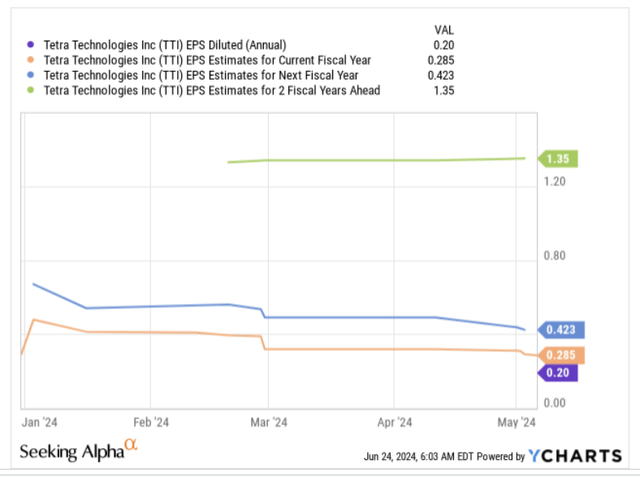

Now, also on the bottom line, it is important to note that TTI is forecast to have even more stable medium-term growth through FY26 (CAGR of 89% over three years).

YCharts

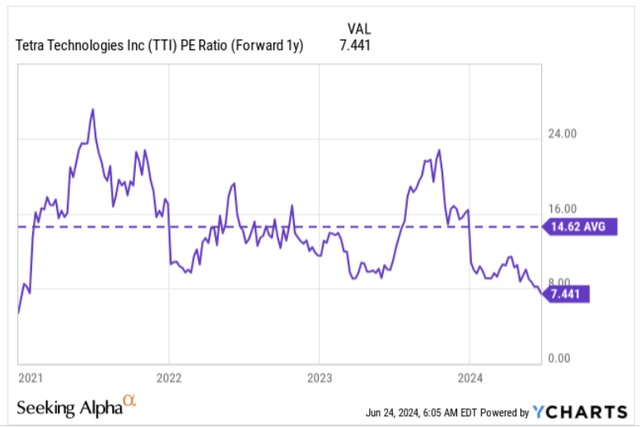

For a company that promises 89% earnings growth, it seems wildly undervalued at a P/E ratio of just 7.44, almost half its 5-year average multiple.

YCharts

FCF increase to support the financing of a brine plant

Even though TTI’s debt levels are at a 3-year high, it’s important to remember that net debt is still very respectable at just 1.5x, so investors don’t have to worry too much about the debt challenges! In addition, TTI’s FCF position, which slipped into negative territory in Q1 (-$29.6 million), will recover significantly over the rest of the year.

First, note that Q1 cash flow was negatively impacted by the timing of revenues, which ultimately impacted the accounts receivable component (in Q1 2024, accounts receivable were nearly $20 million, as opposed to $12.6 million in Q1 2023). Second, note that the company has been adding to its inventory levels in its calcium chloride business, which typically has its strongest quarter in Q2, particularly in Europe (from a revenue perspective), where those inventories are likely to be reduced.

Overall, TTI management believes that despite the adverse first quarter, the established business remains on track to generate positive FCF of over USD 40 million for the full year, which could then prove to be a very useful source of financing for TTI’s Arkansas Brine development project (the Company owns brine leases valued at approximately 40,000 acres with inferred bromine resources of overr 5 million tonnes) and prevent the company from issuing equity to finance these measures.

The desalination option

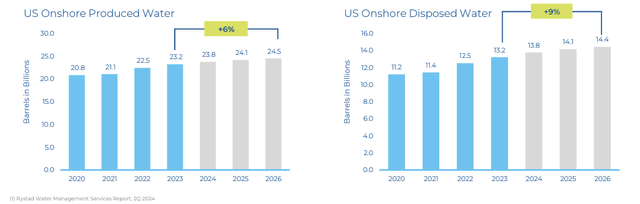

An underrated but promising aspect of the entire TTI story is the company’s ability to use water desalination technology, which will likely be adopted with greater enthusiasm in the Permian Basin. When oil and gas companies produce oil, they also receive groundwater (estimated at 5-6 barrels per barrel of oil), which can then be passed through TTI’s technology to ensure further reuse while extracting valuable minerals. The opportunity to address the problems here is enormous, as onshore wastewater volumes are expected to grow rapidly by 9%, compared to just 6% for produced water.

Q1 Investor Presentation

TTI is taking small steps here and is expected to begin its first commercial desalination contract at a plant in South Texas early next year.

Final Thoughts – Favorable Risk-Reward Ratio on the Charts

YCharts

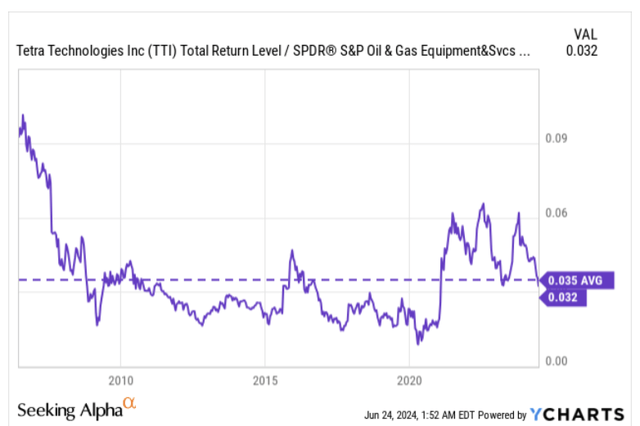

Over the past two decades, TTI’s relative strength as a function of the SPDR Oil and Gas Equipment Services portfolio has averaged around 0.035x. Last year, at the end of the third quarter, things were looking pretty good, with the ratio nearly double the long-term average, dampening the incentive to go long. This is no longer the case, as the ratio has reverted to the mean in recent months and is now trading below its long-term average.

Invest

On the monthly chart of TTI, there is then a risk of acting prematurely, as we still have another week of price action ahead of us that must be reflected in the monthly candle. Nevertheless, we can broadly see that the monthly price prints since late 2018 to date have largely occurred within the confines of the two uptrend lines. Based on the historical performance of the price when reaching the lower trend line, it would not be unreasonable to expect a bottom to form around the current level. In any case, given the distance of the price from the respective trend lines, it is fair to say that the overall risk-reward ratio now appears to be significantly better.

:max_bytes(150000):strip_icc():focal(999x0:1001x2)/jenn-tran-1-070124-0ec516b8d4ab40f580c56e46a998b7cb.jpg)